When you own a home, understanding your home equity is crucial, as it contributes to your net worth and borrowing ability. Simply put, home equity is the value of your home minus your mortgage debt. You can also think of it as the amount of your home that you actually own. You can access this equity to secure loans or lines of credit.

Home equity begins with your first down payment and increases as you pay off your mortgage. Initially, most of your mortgage payment goes toward interest, but over time, more goes toward the principal, building your equity. This equity can be a significant financial asset and can be used as collateral for loans with lower interest rates than personal loans. It can also be used for home improvements, debt consolidation, emergencies, or education.

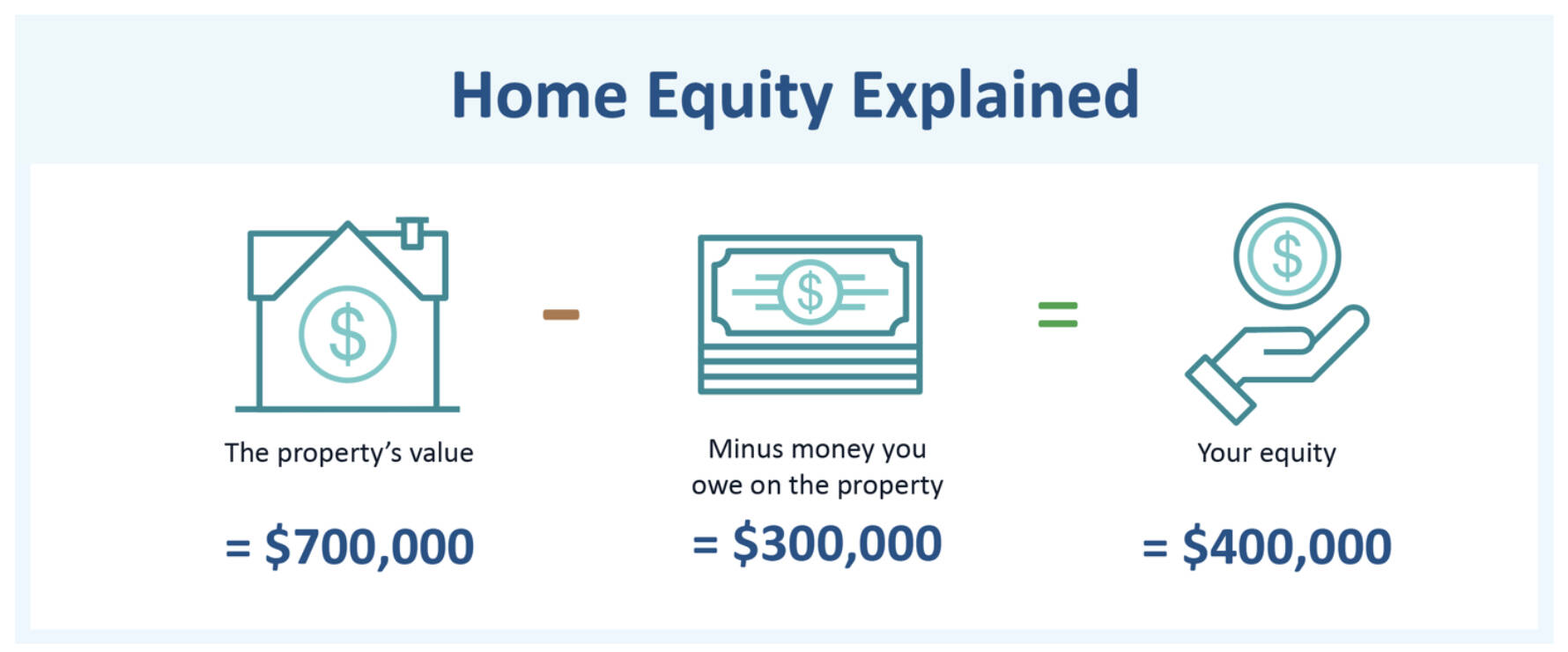

How to calculate home equity

- The first step is to determine your home’s value. Use an estimate from recent sales in your area, online valuation tools, or consult a real estate agent to determine your home’s current market value.

- Then, calculate your total debt. Look at your mortgage balance, as well as any second mortgages or home equity loans, to get a full picture of what you owe.

- Finally, subtract your debt from your home’s value. Use the formula: Home Value – Total Debt = Home Equity.

Example calculation: If your home is worth $700,000 and you owe $300,000 on your mortgage, your equity is $400,000.

It’s important to remember that since home values are tied to market conditions, your equity will fluctuate with changes in the housing market. This means your borrowing power may increase or decrease over time.

How much can you borrow?

Lenders use a loan-to-value (LTV) ratio to determine how much you can borrow. To calculate LTV, divide your equity value by the loan amount and multiply by 100. For example, if your home is worth $400,000 and your mortgage is $240,000:

$240,000 / $400,000 = 0.60 (or 60% LTV)

Lenders typically allow borrowing up to 80% of the home’s value. In this case, 80% of the home value ($320,000) minus the amount owed ($240,000), means you could access $80,000.

There are three primary ways to borrow against your equity:

- Mortgage: A loan to purchase or refinance your home, which may include a cash-out refinance to access equity if interest rates have decreased.

- Home Equity Line of Credit (HELOC): An open-ended loan that allows you to borrow amounts up to a set limit. You only pay interest on the amounts you take out during the draw period. When the draw period ends, any outstanding amount withdrawn from your home equity line of credit (HELOC) will become a fixed rate loan, and you will make monthly principal and interest payments.

- Home Equity Loan (HELOAN): A traditional loan with fixed interest rates. You borrow a specific loan amount, receive a lump sum up front, and then make regular payments during a fixed repayment period.

Home equity is a valuable financial asset that can be leveraged for various purposes, but it’s essential to borrow wisely and understand the risks involved. Determining whether it is a good idea to borrow against your home equity depends on your financial needs and how you plan to use the money.

If the funds are for home improvements or emergencies, it might make sense. However, borrowing for luxury expenses can be risky, as your home is at stake. Consider all financing options, compare interest rates, and choose the product that aligns with your financial goals.

If you still have questions on whether a home equity solution is right for you, the First Fed mortgage team is happy to help you find the best solutions for your financial goals. Or, if you are ready to get started, you can apply online for a Home Equity Loan or Line of Credit.

First Fed is a member FDIC and Equal Housing Lender.